How much of Black Hills Energy's price hike is state policy responsible for? A two-parter on HB25-1302 a bill creating more gov't and raising homeowner's premiums.

How much of Black Hills Energy's price hike is state policy responsible for?

Let me start with a quote from the Sun article linked below.

"'This has been one of the most difficult cases I’ve had at my time at the PUC as I was moved and deeply concerned by the comments we heard regarding the impact of this rate increase on these customers and communities,' PUC Chairman Eric Blank said in voting for the rate hike. 'At the same time, we clearly have legal and fiduciary duties to the utility that limit and constrains us,' Blank said. 'I am really unhappy about raising rates. We have no choice and are doing the best we can do given the $370 million in capital increases in spending.'”

Whether or not you believe Mr. Blank's words above, pay attention to what he says there in the middle regarding the steep rate hike Black Hills Energy is putting on consumers in South Central Colorado cities like Pueblo and Canon City. He says they have a "legal and fiduciary" duty to the utility.

Put more plainly, he's saying the PUC's hand was forced: they cannot legally vote to make Black Hills eat the costs they're incurring, and they can't let Black Hills NOT do the construction projects they're planning.

How'd we end up here? There are two dynamics at play here in my view.

One, we humans are terrible about paying for things ahead of time. What I mean is that we have an awful habit in this country of not paying replacement costs as we go. You see it time and time again in infrastructure.

Two, put simply, this state elected Democrats who march in lockstep with rabid environmentalists who see nothing but their environmental concerns (and have the resources to live comfortably regardless of the restrictions they put in place).

We elected Democrats who put into place energy mandates and grid requirements for utilities and customers, rules that drive prices up in the name of "clean energy".

And we elected Democrats who had the foresight to make sure that the deciding body, the public face of these rate increases was not themselves, but an unelected board. A board that can sincerely (or not) say that they had to do what they did in the face of large public opposition.

Undoubtedly part of the cost increases here will be due to replacing older equipment and modernizing. But I hope the Black Hills Energy customers save some of their frustration for the other group that has cost them money.

It's not Black Hills or the PUC per se. It's the folks who forced their hand.

It's the Democrats in the state capitol and in the governor's chair.

https://coloradosun.com/2025/03/14/electric-bill-increase-black-hills-energy-canon-city-pueblo-florence/

HB25-1302 should be named "Increase Homeowner's Insurance Premiums" PART 1 of 2

HB25-1032, linked first below, actually carries the name "Increase Access Homeowner's Insurance Enterprises", but if you read the bill, what it will ultimately do is make it costlier to get homeowner's insurance while at the same time creating yet more government enterprises.**

It will grow government. It will end with more unaccountable and unelected bureaucrats in Colorado deciding what to do with your money.

This is a big enough bill that it's going to take two posts to properly digest. This is post 1 of 2 and will be about the first enterprise. The second enterprise, I will take on in post 2 of 2 (following this one).

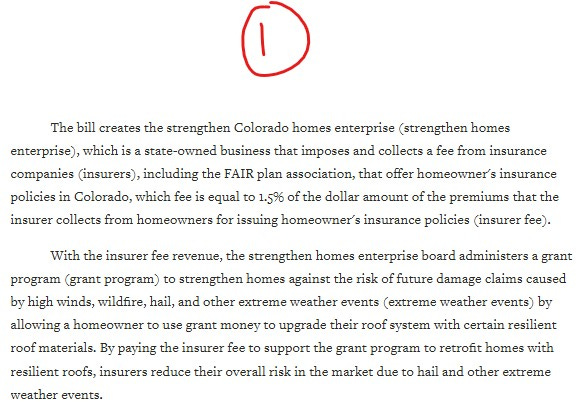

Screenshot 1 comes from the bill's summary.

It lists how the "Strengthen Homes Enterprise" will get its revenue and what it will be spending it on. This enterprise will charge your insurance company 1.5% of your homeowner's insurance and then use that money to administer a grant program where the proceeds are doled back out in the form of grants to help homeowners to upgrade their roofs to hail-resistant shingles.

Who decides who gets that sweet, sweet, government money? The enterprise's appointed board will. I couldn't find specific language in the bill requiring one criteria or another.

I said at the top that this bill should be called the raise homeowner's insurance costs because, while the fees are tacked onto homeowner's insurance companies, guess who ultimately ends up paying these costs? Consumers, that is, you and I.

The cost for this grant program will come from increased premiums that you and I pay.

We had a pretty bad hailstorm up where I live in 2019 (if memory serves). When it came time to replace the roof, my wife and I decided to go with hail resistant shingles. This is Colorado. Hail happens and I didn't want to have this hassle over and over.

In addition to the convenience, our homeowner's insurance company offered a discount. The shingles did cost us extra, but I calculated that 4 years without replacement would make the upgraded shingles pay for themselves; a winning gamble it turned out.

The point here is that private, market-based incentive programs already exist to encourage people to upgrade their roofs. So what is this government program for? What problem does it solve?

Pretty easy to see that one. This is yet another (Democrat) wealth transfer. It's using government to take from some to give to another. It raises homeowner's insurance rates so that others can upgrade.

Who will that be? Too early to tell. It will depend on how the unelected board does things. Maybe it will be lower-income houses. Maybe it will be (like our state's welfare for the wealthy EV program) for the rich.

It gets even weirder in part 2. See you there.

**As a refresher if needed: a government enterprise is a quasi-business the government sets up. This enterprise charges a fee for some sort of service provided (whether or not you get this service, whether or not it has value to you is another question). The reason politicians of both parties love them is that the money enterprises bring in is completely free of TABOR restrictions and/or free of needing your approval to impose.

https://leg.colorado.gov/bills/hb25-1302

HB25-1302 should be named "Increase Homeowner's Insurance Premiums" PART 2 OF 2.

As I mentioned in part 1, HB25-1032 (linked first below for convenience) creates two new enterprises for Colorado. Enterprises which grow our government, cede yet more authority to unelected boards, and which will end up costing consumers more.

If you didn't read the previous post (part 1 of 2) about the first enterprise created by HB25-1302, go back and give it a look. You don't need to do it prior to reading this part, but a full understanding of the bill requires both.

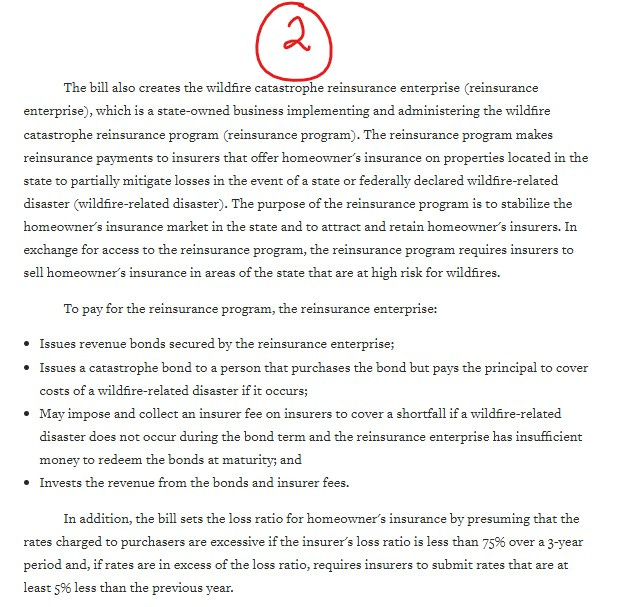

Screenshot 2 comes from the HB25-1032's summary.

It details the creation and duties of the second enterprise created, the "Wildfire Catastrophe Reinsurance Program Enterprise". Beware: this will get complicated, so stay with me.

Let's first touch on some prerequisite material. Reinsurance is when an insurance company purchases or receives coverage against its biggest losses. E.g. our state has a reinsurance program for health insurance in the individual market whereby health insurance companies agree to keep their premiums lower if the State of Colorado agrees to cover the biggest and costliest claims (those above a certain dollar threshold).

See more context in an earlier newsletter linked second below.

A wildfire reinsurance program would then offer homeowner's insurance companies a chance to join in the program. If they do, their largest potential losses would be covered by this government enterprise. The cost for this service is that the insurance companies would have to offer wildfire insurance in this state, pay fees, and also have caps on the premiums they can charge (see the bottom part of screenshot 2).

Money don't grow on trees, so how will this all be funded? Here's where the complications come in. Aren't our legislators clever in naming and funding things?

I'll be as brief as I can in listing the steps.

-- The Reinsurance Enterprise will issue revenue bonds to those that want to buy them. The State of Colorado backs the repayment of these bonds with revenue from the Enterprise.

-- Investors that buy these bonds are making a bet. They are betting that no wildfire will happen. If no catastrophic fire that requires reinsurance happens, they will get their money back with interest (and a pretty good amount compared to other bonds considering the risk).

-- The insurance companies and the Reinsurance Enterprise are betting that a disaster will happen. If it does, the investors that purchased the bonds don't get their money back. The proceeds raised from the sale of the bonds is what funds the reinsurance and covers the losses from the fire.

--Essentially what happened is that this scheme allows the Colorado and the insurance companies to put their risk into the bond market (whereas before insurance companies had to prepare for a loss by raising insurance rates or, as in the case of the health reinsurance, by putting those costs directly on Coloradans).

--Any revenue needed to make up a shortfall in the Reinsurance Enterprise (say no wildfire happens and you have to pay off the investors of your bonds) is gained by assessing fees on homeowner's insurance companies that participate in the program.

Phew!

That last bullet point above is the one that is operative here, at least as far as consumers are concerned. I am not financial wizard enough to speak too confidently here, but there is perhaps a way for this program to become self-sustaining after a few years.

The fact is, however, that until that happens, the insurance companies in this program will make up the difference. A difference that will be passed through to consumers. Just like with our state's health plan reinsurance scheme, the money has to come from somewhere. If it isn't taxpayers (as it is with health reinsurance), it will be from homeowner's insurance consumers.

Further, this program voluntary. The legislative declaration on the bill makes it clear that they are trying to convince insurers to stay in Colorado by offering reinsurance, but I wonder if the insurance companies see this as a plum deal. If this program isn't popular, that means high costs spread among fewer insurance companies.

On balance, this bill has good intentions. It sets out to do good things.

Having hail (and/or fire) resistant roofs is a good idea. In the long run it saves everyone money.

Having wildfire insurance in this state is a good idea.

But we shouldn't be socializing these costs and that goes double for doing by growing our government and creating yet more unaccountable state entities.